Selected Slides from Mary Meeker's 2018 Internet Report

(with Commentary)

I excerpted the slides below from Mary Meeker's slide deck from May 2018 which can be found here. Update (June 6, 2020): This link doesn't work anymore. Here's a link that works and provides access to reports from all years.

I have preceded each slide with my own commentary.

I've also included some predictions based on what the data is telling me. In so doing, we will see in due time whether and to what extent I may have made a fool out of myself! You can find them by looking for the word "predict" highlighted in yellow.

List of revisions:

Aug. 3, 2018: I have commented on the first 9 slides alone. 32 more slides to go. Proof-reading pending.

June 5, 2020: I never commented on the remaining 32 slides. However, I did make all slides X-large for more easy viewing.

June 5, 2020: I never commented on the remaining 32 slides. However, I did make all slides X-large for more easy viewing.

----------

Global Technology Private Financing

The next chart shows how technology private financing seems to have undergone a regime change in 2014. Its dollar amount somewhat doubled from the preceding 3 years.

From 2009 (NASDAQ low point) to 2013, the stock market more than doubled. My hypothesis is that investors took their profits from the stock market and in 2014, stepped up their pace of investment in the private markets.

The lesson from 2000 is seen to be that while the stock market fell through 2002, private technology financing also fell, and it fell for one more year beyond 2002. Today, this should serve as a warning sign to private companies expecting to raise private funds in the event that the public stock markets turn sour.

USA Public Company R&D + Capital Expenditures

The next chart shows the massive amount of capital spent by US public companies on R&D plus Capital Expenditures in a single year. The figures run in the tens of billions of dollars on a per-company basis and the aggregate amount is almost $300 billion.

Also observe how Facebook falls short relative to other high tech names most of which are the FAANG stocks.

Square

The next slide is about Square, ticker SQ. Its global active seller count was 2.8 million estimated as of 2017.

The average GPV (Gross Payment Volume) per seller works out to $23,000 rounded for the year 2017. (These are small sellers.)

Shopify

The next slide is about Shopify, ticker SHOP. Its global active merchant count was 609,000 estimated as of 2017.

The average GMV (Gross Merchandise Value) per merchant was $40,000 rounded for the year 2017. (These are small merchants.)

Mobile App Session Growth

The following chart shows Mobile App Session Growth by App Type.

Shopping-related app sessions exhibit the fastest one-year growth. (A single year might be too short to establish a long-term trend, perhaps.)

The footnote says that the results are based on tracking 1 million apps across 2.6 billion mobile devices.

E-commerce Sales

The next chart is about e-commerce sales level and growth. The level is at $450 billion in 2017, up from half that level 5 years prior. This implies a 5-year growth rate of 15% per year, which is in line with the displayed growth rate.

Physical Retail Sales

The next chart is about physical retails sales level and growth. (If we've looked at e-commerce sales, it would be relevant to look at physical retail sales because of all the talk that e-commerce is eating away at retail.)

The level here is displayed as $3 billion in 2017 (but I'm guessing that there's an error in the scale and that it's really "trillion" and not "billion". For supporting evidence, see here).

The more crucial point is that retail sales growth has been less than 3% per year whereas e-commerce sales growth has been 15% per year or 5 times higher growth rate.

However, e-commerce's 15% growth rate is based on a smaller base than retails 3% growth rate, meaning that e-commerce's 15% growth rate translated into $62 billion of sales growth whereas retail's 3% growth rate translated into $152 billion. (Looking only at growth rates did not provide a complete picture!)

The final thing to notice is that retail's growth rate is decelerating. (Note the downward sloping trend line in red.) I'm not convinced that e-commerce's growth rate is decelerating. By looking at data at the other referenced source, I note that under a constant growth rate, since the level of sales increases year over year, the dollar amount of sales growth has been increasing year over year. To drive home the point, the retailer needs more resources to handle a 15% sales growth rate in year N+5 than in year N, say.)

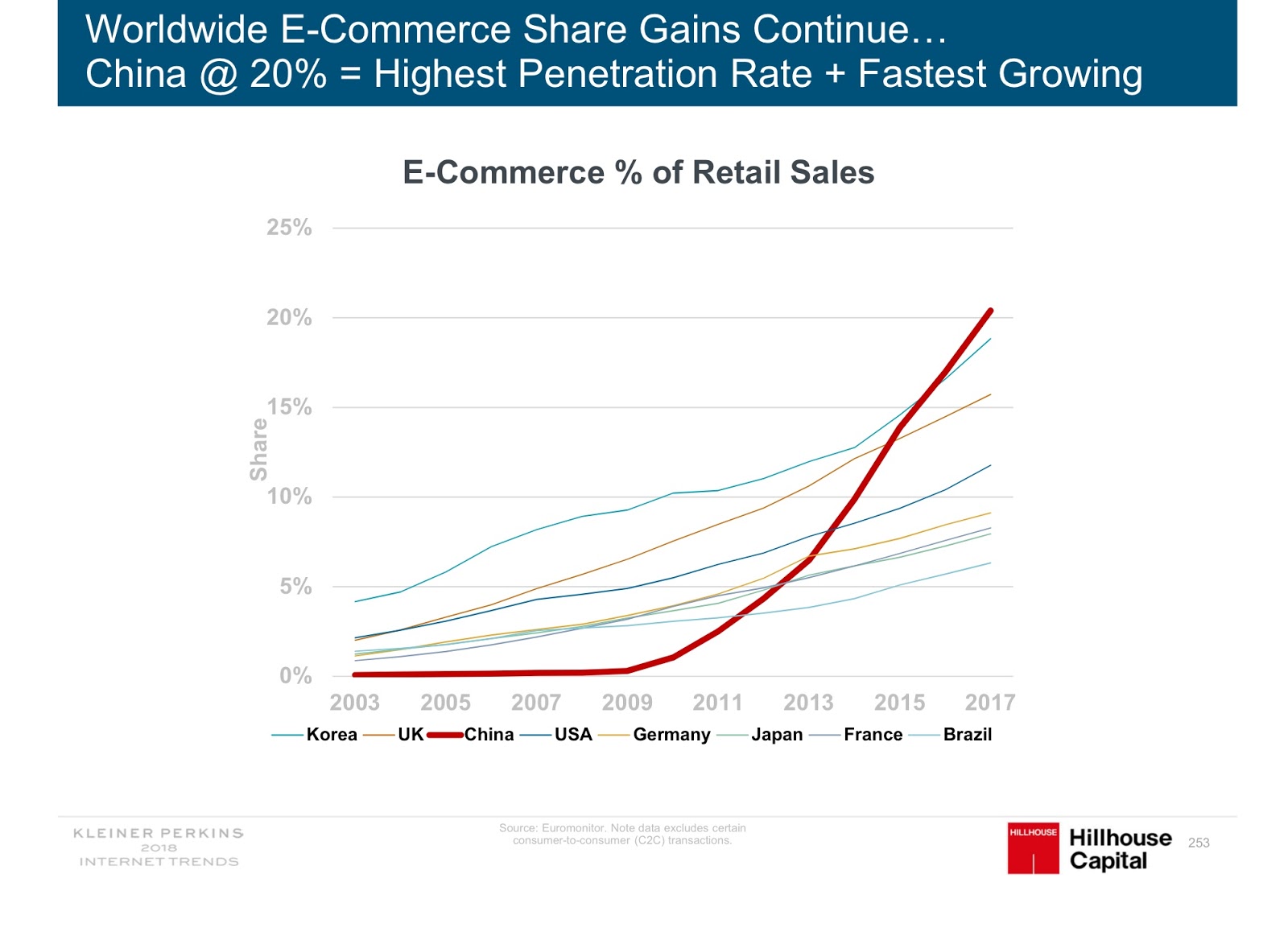

E-commerce vs Physical Retails Sales

The next chart shows that e-commerce sales is growing relative to retail sales. In the 10 years from 2007 to 2017, e-commerce sales grew from 5% of retail sales to 13%.

At the same pace, it will take 11 more years before e-commerce sales reach the level of retail sales. (Let me do a sanity check on this. We have e-commerce sales at $450B in 2017 and retails sales at a level that's in the trillions. Using the other source referenced above, I back out a figure of $4.5 trillion for annual retail sales. I ask, what is the growth rate associated with going from $450B to $4.5T in 11 years? This is a 1000X increase! Answer: 87% per year. However, in the 5 years ending in 2017, e-commerce's growth rate has been 15%. So, is it possible that this growth will accelerate and rise to 87% per year? I doubt it. I think what will happen is that the $4.5T associated with retail sales will fall after the 11 years are up. Think about it. The consumers in the US have a limited capacity for consuming. It's this consumption that corresponds to e-commerce and retail sales. Today, their aggregate consumption amounts to the sum of e-commerce sales plus retail sales, a figure which equal $450B + $.5T i.e. $4.95 trillion or $5 trillion rounded. Now, in 11 years time, we might end up in a situation where e-commerce sales represent 100% of retail sales, but with the added case that e-commerce sales amount to half of the $5T figure i.e. $2.5T and with retail sales also amounting to the same amount. In this case, e-commerce sales will have to grow from $450B to $2.5T in 11 years. The growth rate associated with this happens to be ... 77% per year. This 77% growth rate is still too high to be realistic, I think. So, I'm going to make a prediction, and in so doing, perhaps make a fool out of myself. I predict that if the trends from the 5 years ending with 2017 were to continue, it would take longer than 11 years for e-commerce sales to reach the same level as retail sales. Let's come back in 11 years, i.e. 2029, and check to see what happened.)

Amazon & Alibaba

The next slide shows two behemoths next to one another. They are in the same space but in different geographic regions. Amazon and Alibaba.

Alibaba's higher GMV-to-Revenue ratio relative to Amazon's means that there are more third-party sellers on Alibaba than Amazon.

I checked their P/S ratio (price-to-sales) and stock prices. They are as follows.

AMZN P/S = 4.3 vs BABA at 12.5. The market sees more revenue growth potential in BABA. (I take this back! It seems misleading to work with "Revenue" given that Revenue doesn't capture "GMV". I'll pick this up a few lines below.)

AMZN stock price = $1,821 vs BABA at $180.

AMZN market cap = $880 Bn vs BABA at $468 Bn.

As of Aug. 3, 2018.

Picking up where I left off a few lines above, the interesting question is, which stock is cheaper? Both seems to have similar growth rates, with Alibaba's being slightly better. Let's assume that this trend continues, which means that growth won't cause any difference in valuation.

We could look at the ratio of market cap to GMV, in which case Alibaba comes out cheaper. Alternatively, we could look at the ratio of market cap to Free Cash Flow. Again, Alibaba comes out cheaper. So, I'll make the following prediction.

Barring the impact of currency on stock returns (i.e. assuming that we hedge away currency risk), I predict that Alibaba's stock price will outperform Amazon's stock price over, say, the next 5-10 years.

P.s. I think I need to qualify / modify my prediction by taking into account any differences in their R&D budgets ...

Author is also on Twitter

No comments:

Post a Comment